Elevate Your Practice: Essential Technology Tips for Modern Accounting Firms

Looking for expert accounting tech tips to transform your practice? These accounting tech tips will boost your firm’s efficiency, security, and client service. Discover essential accounting tech tips that modern firms use to stay competitive, from cloud migration to AI-powered automation.

Discover 5 essential tech tips to streamline operations, enhance security, and drive growth instantly with GiaSpace.

| Fact/Metric | Value | Source/Date |

| Avg. Efficiency Gain (Automation) | Up to 40% | Industry Studies, 2024 |

| Data Breach Cost (SMB Avg.) | $165,000 | IBM Cost of a Data Breach Report, 2024 |

| GiaSpace IT Solutions Experience | 20+ Years in Tech | GiaSpace Company Info |

Why These Accounting Tech Tips Matter Now

The accounting tech tips in this guide aren’t theoretical—they’re battle-tested strategies that leading firms use daily. These accounting tech tips address the most pressing challenges facing modern practices: efficiency bottlenecks, cybersecurity threats, and evolving client expectations. Whether you’re just beginning your digital transformation or looking to optimize existing systems, these accounting tech tips provide actionable pathways to measurable results.

Foundational Accounting Tech Tips: Understanding the Technology Imperative

The accounting profession is undergoing a profound transformation, making accounting tech tips more critical than ever. The first of our accounting tech tips: understand that technology is no longer optional. These accounting tech tips begin with recognizing why digital transformation is a strategic imperative for survival and growth.

Here’s why technology is no longer a luxury but a necessity for today’s accounting firms:

- Staying Competitive: Clients now expect their accounting firms to be efficient, accessible, and digitally savvy. Firms clinging to outdated methods risk losing clients to competitors who leverage technology for faster, more accurate service.

- Meeting Client Expectations: Today’s clients are digitally native. They expect seamless online interactions, secure document sharing, and real-time access to their financial data. Technology enables you to meet and exceed these evolving demands.

- Enhancing Efficiency and Accuracy: Manual data entry and repetitive tasks are prone to human error and consume valuable time. Technology automates these processes, significantly improving accuracy and freeing up your team for higher-value, advisory work.

- Robust Data Security: Accounting firms handle some of the most sensitive financial data. With cyber threats constantly escalating, robust technology is your first line of defense, protecting both your firm’s reputation and your clients’ invaluable information.

- Enabling Remote Work and Flexibility: The modern workforce demands flexibility. Cloud-based technologies empower your team to work securely and efficiently from anywhere, attracting top talent and ensuring business continuity.

- Driving Strategic Insights: Beyond compliance, technology, particularly data analytics and AI, allows firms to extract deeper insights from financial data, offering proactive advice that elevates your role from number-cruncher to trusted business advisor.

- Compliance and Regulation: The regulatory landscape is constantly shifting. Technology can help automate compliance checks, maintain meticulous audit trails, and ensure your firm remains aligned with the latest legal requirements.

In essence, technology empowers accounting firms to work smarter, serve clients better, and position themselves for long-term success in an increasingly digital world.

Accounting Tech Tip #1: Leverage Cloud Accounting Software for Maximum Efficiency

Key Accounting Tech Tips for Cloud Adoption:

- Choose cloud platforms with accounting-specific features

- Prioritize real-time collaboration capabilities

- Ensure automatic backup and update functionality

- Verify multi-device accessibility for remote work

Our first major accounting tech tip focuses on cloud migration. Among all accounting tech tips, adopting cloud accounting software delivers the most immediate, measurable impact. This accounting tech tip transforms how your firm manages finances, interacts with clients, and collaborates internally.

Here’s how cloud accounting software instantly elevates efficiency and collaboration:

- Anywhere, Anytime Access: This is the most immediate benefit. Cloud software allows your team and clients to securely access financial data, ledgers, and reports from any device with an internet connection. No more being tied to a single office computer or struggling with outdated desktop software. This flexibility is crucial for remote work and serving a diverse client base.

- Real-Time Data and Insights: Forget waiting for month-end closes or struggling with outdated spreadsheets. Cloud platforms provide real-time updates on financial transactions and performance. This means your clients have an up-to-the-minute view of their financial health, and you can offer timely, proactive advice.

- Seamless Collaboration: Cloud accounting breaks down traditional silos. Your internal team can work concurrently on the same files, reducing version control issues and improving teamwork. Furthermore, you can grant secure access to clients, allowing them to upload documents, review reports, and communicate directly within the platform.

- Automated Updates and Backups: Reputable cloud providers handle all software updates, maintenance, and data backups automatically. This frees your IT staff (or your time) from these burdensome tasks, ensuring you’re always on the latest, most secure version, and your data is protected.

- Enhanced Data Security: Counter-intuitively, cloud environments are often more secure than on-premise solutions for most small to medium-sized firms. Cloud providers invest heavily in enterprise-grade security measures, encryption, multi-factor authentication, and regular audits that would be cost-prohibitive for individual firms.

- Scalability and Flexibility: As your firm grows or your client needs change, cloud accounting solutions can easily scale up or down. You can add or remove users and features with ease, ensuring your software evolves with your practice without major overhauls.

By embracing cloud accounting, your firm gains unparalleled agility, security, and the ability to deliver superior service, making you a more valuable and responsive partner to your clients.

Accounting Tech Tip #2: Automate Bookkeeping and Data Entry to Free Up Strategic Time

This accounting tech tip revolutionizes daily operations. Among critical accounting tech tips, automation ranks highest for immediate time savings. This accounting tech tip isn’t about replacing accountants—it’s about empowering them to focus on strategic, high-value advisory work instead of repetitive data entry.

The transformative benefits of automation include:

- Significant Time Savings: Imagine the hours your team currently spends on repetitive tasks like categorizing transactions, reconciling accounts, and inputting data from receipts and invoices. Automation tools can perform these tasks in seconds, freeing your staff to focus on analysis, client advisory, and complex problem-solving.

- Reduced Human Error: Manual data entry is inherently prone to mistakes. Even the most diligent accountant can make a typo. Automation minimizes these errors, leading to cleaner, more accurate financial records and reports, which is critical for compliance and client trust.

- Real-Time Financial Visibility: Automated systems can instantly pull data from bank feeds, credit card accounts, and other sources. This means financial records are updated in real-time, providing immediate insights into cash flow, expenses, and profitability, rather than waiting for manual processing.

- Improved Compliance and Audit Trails: Automation tools can enforce consistent data entry and categorization rules, ensuring better adherence to accounting standards. They also create comprehensive, immutable audit trails, making compliance checks and audits smoother and faster.

- Cost-Effectiveness: While there’s an initial investment, the long-term cost savings from reduced labor, fewer errors, and increased efficiency can be substantial. Your team can handle more clients without proportional increases in headcount, boosting your firm’s profitability.

- Enhanced Scalability: As your client base grows, automated systems can handle increasing volumes of transactions without a corresponding increase in manual workload. This allows your firm to scale efficiently and take on more business.

- Empowered Staff: By offloading mundane tasks, automation allows your accounting professionals to engage in more stimulating, value-added work. This improves job satisfaction, reduces burnout, and helps retain top talent.

Automated bookkeeping and data entry are game-changers, enabling accounting firms to operate with unprecedented efficiency, accuracy, and strategic focus.

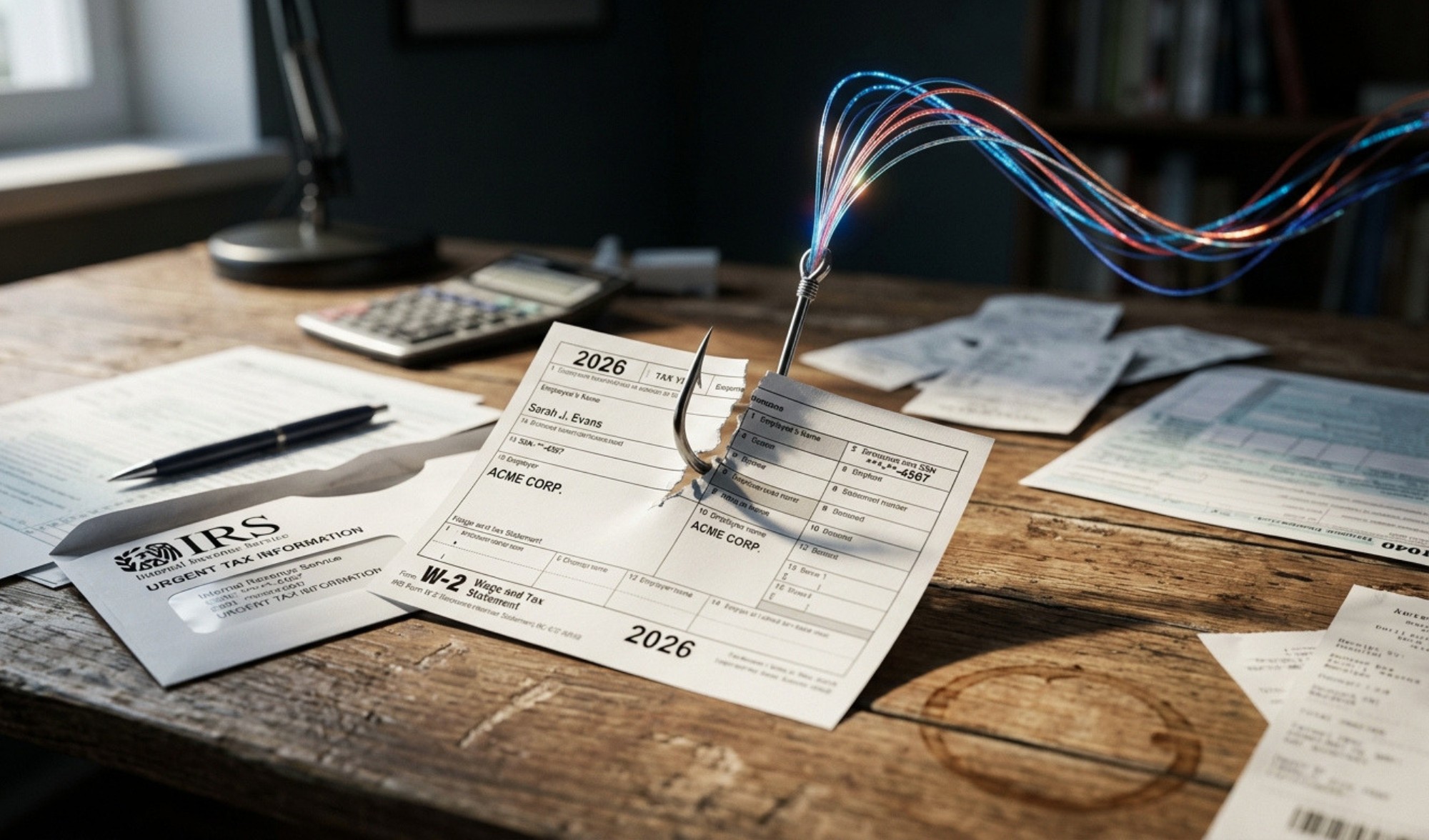

Accounting Tech Tip #3: Implement Multi-Layered Cybersecurity Protection

This accounting tech tip could save your practice from catastrophic losses. Of all accounting tech tips, cybersecurity deserves your immediate attention. This accounting tech tip addresses the reality that accounting firms are prime targets for cybercriminals, making robust security measures non-negotiable.

Here’s how robust cybersecurity measures safeguard your firm and clients:

- Protecting Confidential Client Data: This is paramount. Cybersecurity measures like encryption, secure client portals, and strict access controls ensure that sensitive financial statements, tax records, and personal identification information remain confidential and inaccessible to unauthorized parties.

- Maintaining Client Trust and Reputation: Your firm’s reputation is built on trust. A data breach erodes that trust instantly. Proactive cybersecurity demonstrates your commitment to protecting client data, reinforcing your reliability and professionalism.

- Ensuring Regulatory Compliance: The accounting industry is subject to stringent data protection regulations (e.g., GDPR, HIPAA if dealing with healthcare clients, state-specific privacy laws). Robust security practices help your firm meet these legal requirements, avoiding hefty fines and legal battles.

- Preventing Financial Loss and Business Disruption: Cyberattacks like ransomware can halt operations, encrypt critical data, and demand large ransoms. Strong cybersecurity prevents such attacks, ensuring your firm remains operational and avoids significant financial losses and downtime.

- Mitigating Internal Threats: Not all threats come from outside. Cybersecurity also includes measures like user access management, employee training, and monitoring to protect against accidental data exposure or malicious insider activity.

- Continuous Threat Detection and Response: Advanced cybersecurity solutions provide 24/7 monitoring, threat detection, and rapid incident response capabilities. This means potential threats are identified and neutralized quickly, minimizing their impact.

- Securing Remote Work Environments: As more firms adopt hybrid or remote work models, securing endpoints (laptops, mobile devices) and remote access points becomes vital. Cybersecurity tools like VPNs, secure remote desktop solutions, and endpoint protection ensure data is safe regardless of where your team works.

Investing in robust cybersecurity is an investment in your firm’s future, ensuring the integrity of your operations and the invaluable trust of your clients.

Accounting Tech Tip #4: Leverage Data Analytics and Business Intelligence for Strategic Advisory

This accounting tech tip elevates you from number-cruncher to strategic advisor. Among transformative accounting tech tips, data analytics and business intelligence tools unlock the most competitive differentiation. This accounting tech tip enables you to offer proactive, insights-driven advisory services that clients truly value.

Here’s how data analytics and BI enhance your firm’s insights:

- Deeper Financial Insights: Instead of just reporting what happened, data analytics allows you to understand why it happened. You can identify trends, anomalies, and underlying drivers of financial performance, providing a more comprehensive view of a client’s financial health.

- Proactive Client Advisory: Armed with better insights, you can shift from being a reactive service provider to a proactive advisor. Spot emerging challenges (like declining cash flow or unusual spending patterns) or opportunities (like tax optimization strategies) for your clients before they become critical.

- Enhanced Forecasting and Budgeting: BI tools can analyze historical data to create more accurate financial forecasts and budgets for your clients. This empowers them to make more informed business decisions, allocate resources effectively, and plan for future growth with greater confidence.

- Fraud Detection and Risk Mitigation: Advanced analytics can identify suspicious patterns or anomalies in large datasets that might indicate fraudulent activity or financial irregularities. This adds a crucial layer of security and helps mitigate financial risks for your clients.

- Operational Efficiency for Your Firm: Beyond client insights, BI tools can analyze your firm’s own operational data – billable hours, client profitability, service delivery times – to identify bottlenecks, optimize workflows, and improve your firm’s own efficiency.

- Visualizing Complex Data: Data visualization features within BI tools transform complex numerical data into easy-to-understand charts, graphs, and dashboards. This makes it simpler for both your team and your clients to grasp key financial trends and insights quickly.

- Personalized Client Services: By understanding a client’s unique financial patterns and business drivers, you can tailor your services and recommendations to their specific needs, leading to stronger relationships and increased client satisfaction.

Embracing data analytics and business intelligence positions your accounting firm as a forward-thinking, strategic partner, invaluable to your clients’ success.

Accounting Tech Tip #5: Deploy Client Portals for Secure, Seamless Communication

This accounting tech tip directly impacts client satisfaction and retention. Among client-facing accounting tech tips, secure portals deliver the most immediate experience improvement. This accounting tech tip addresses the modern client’s expectation for 24/7 access, secure document exchange, and transparent communication.

Here’s how these tools elevate your client relationships:

- Secure Document Exchange: Client portals provide a highly secure, encrypted environment for sharing sensitive financial documents (tax forms, financial statements, payroll data) that far surpasses the security of email. This protects client data and ensures compliance.

- Centralized Communication Hub: No more sifting through endless email threads. A client portal acts as a single, centralized platform for all client communications, queries, and document sharing. This creates a clear, organized record of all interactions.

- Enhanced Convenience and Accessibility: Clients can access their documents and communicate with your firm 24/7 from any device. This convenience improves their experience and allows them to engage with your firm on their own schedule.

- Streamlined Workflows: Portals often include features for task management, digital signatures, and automated reminders. This streamlines the back-and-forth for information gathering, approvals, and project updates, making processes faster and more efficient for both sides.

- Improved Transparency: Clients can log in and see the status of their projects, uploaded documents, and communication history. This transparency keeps them informed and reduces the need for constant status update requests.

- Professional and Branded Experience: A well-designed client portal provides a professional, consistent, and branded experience for your clients, reinforcing your firm’s commitment to modern service and data security.

- Faster Response Times: Integrated communication tools within portals can facilitate quicker responses by directing queries to the right team member and centralizing discussions, leading to higher client satisfaction.

- Reduced Administrative Burden: By automating reminders and providing self-service options for clients, your administrative staff can spend less time on routine follow-ups and more time on high-value tasks.

Client portals and communication software are essential tools for building stronger, more efficient, and more trusted relationships with your accounting firm’s clients.

How can AI and Machine Learning transform accounting firm operations?

Artificial Intelligence (AI) and Machine Learning (ML) are not just buzzwords; they are rapidly becoming integral to the future of accounting. These technologies are poised to fundamentally transform how accounting firms operate, automate complex tasks, and unlock unprecedented levels of insight. Far from replacing accountants, AI and ML empower them to perform at a higher, more strategic level.

Here’s how AI and ML can revolutionize your accounting firm:

- Hyper-Automation of Repetitive Tasks:

- Data Entry & Categorization: AI-powered OCR (Optical Character Recognition) can extract data from invoices, receipts, and bank statements with remarkable accuracy, automating reconciliation and transaction categorization. This eliminates manual data entry errors and frees up countless hours.

- Invoice Processing: Automate the entire invoice lifecycle, from receipt to payment, including matching invoices to purchase orders and identifying discrepancies.

- Payroll & Expense Management: AI can streamline payroll calculations, tax deductions, and expense report processing, ensuring accuracy and compliance.

- Enhanced Fraud Detection and Anomaly Spotting: ML algorithms can analyze vast datasets to identify unusual patterns or anomalies in financial transactions that might indicate fraud, errors, or other financial risks far more effectively than human review alone. This proactive detection protects your clients and your firm.

- Predictive Analytics and Forecasting: AI can leverage historical data to generate highly accurate financial forecasts, cash flow predictions, and revenue projections. This moves accounting from historical reporting to forward-looking strategic guidance for clients.

- Smart Auditing: AI can automate the sampling and analysis of large volumes of transaction data, identifying high-risk areas for auditors to focus on. It can also aid in compliance checks and flag potential regulatory issues.

- Natural Language Processing (NLP) for Document Analysis: AI can process and summarize large financial documents, contracts, and regulatory texts, saving time on research and compliance verification. It can even assist in drafting financial reports and internal memos.

- Personalized Client Service (Chatbots/Virtual Assistants): AI-powered chatbots can handle routine client queries, provide instant answers to common questions, and guide clients to relevant resources within your portal, improving response times and freeing up your staff.

- Continuous Learning and Improvement: ML models learn from new data and interactions, continuously improving their accuracy and efficiency over time. This means your automated processes get smarter and more effective with use.

Embracing AI and ML isn’t just about efficiency; it’s about gaining a significant competitive edge, allowing your firm to deliver deeper insights, greater accuracy, and more strategic value to your clients.

What are the key considerations for implementing new technology in an accounting firm?

Implementing new technology in an accounting firm isn’t just about purchasing software; it’s a strategic undertaking that requires careful planning to ensure a smooth transition and maximize your return on investment. Without thoughtful consideration, even the most advanced tools can fail to deliver their promised benefits.

Here are the key considerations for successful technology implementation:

- Define Your Goals Clearly: Before you even look at solutions, ask: What specific problems are we trying to solve? Are we aiming to reduce manual errors, improve client communication, enhance cybersecurity, or enable remote work? Clear, measurable goals will guide your selection process.

- Assess Your Current Infrastructure: Understand your existing hardware, software, and network capabilities. Will new technology integrate seamlessly, or will significant upgrades be required? Compatibility is crucial.

- Data Migration Strategy: Moving existing financial data can be complex. Plan a robust data migration strategy, including data cleansing, backup procedures, and testing, to ensure data integrity and minimize disruption during the transition.

- Security and Compliance: Given the sensitive nature of accounting data, security must be paramount. Ensure any new technology adheres to the highest security standards (encryption, MFA) and helps your firm maintain compliance with relevant industry regulations.

- User Adoption and Training: Technology is only as good as its users. Develop a comprehensive training program for your staff, addressing different skill levels. Foster a culture that embraces change, highlights the benefits for them, and provides ongoing support.

- Scalability for Future Growth: Choose solutions that can scale with your firm. Will the technology accommodate increased client loads, new services, or additional staff without requiring another complete overhaul in a few years?

- Vendor Support and Reputation: Research the vendor thoroughly. What is their track record? What kind of ongoing support do they offer (technical support, training resources, community forums)? A responsive and knowledgeable vendor is critical for long-term success.

- Cost vs. ROI Analysis: Look beyond the initial purchase price. Calculate the total cost of ownership, including implementation, training, and ongoing maintenance. More importantly, project the return on investment in terms of efficiency gains, reduced errors, increased client retention, and new service opportunities.

- Integration Capabilities: Will the new technology integrate seamlessly with your existing essential systems (CRM, payroll, tax software)? Siloed systems create inefficiencies.

- Phased Rollout (Where Applicable): For larger implementations, consider a phased rollout. This allows your team to adapt gradually, provides opportunities for feedback, and minimizes overall disruption.

By addressing these considerations proactively, your accounting firm can make informed technology investments that truly elevate your operations and position you for sustained success.

Quick Reference: 6 Essential Accounting Tech Tips”

These accounting tech tips provide a roadmap for modernizing your practice:

Accounting Tech Tip #1: Migrate to cloud accounting software for anywhere, anytime access and real-time collaboration

Accounting Tech Tip #2: Automate bookkeeping and data entry to eliminate errors and free up strategic time

Accounting Tech Tip #3: Deploy multi-layered cybersecurity to protect sensitive client data and maintain trust

Accounting Tech Tip #4: Leverage data analytics and BI tools to deliver proactive, strategic advisory services

Accounting Tech Tip #5: Implement secure client portals for seamless, professional communication

Each of these accounting tech tips addresses specific operational challenges while contributing to your firm’s overall digital transformation.

How can GiaSpace help accounting firms implement these technology solutions?

At GiaSpace, we don’t just recommend accounting tech tips—we help you implement them. Our team has helped hundreds of accounting firms execute these exact accounting tech tips with measurable results. We understand that reading accounting tech tips is easy; executing them successfully is where most firms need expert guidance.

Here’s how GiaSpace can be your trusted partner in implementing and managing these essential technology solutions:

- Strategic IT Consulting Tailored for Accounting: We don’t just sell software. Our experts begin with a deep dive into your firm’s current IT infrastructure, workflows, and business goals. We then provide tailored recommendations for the best-fit cloud accounting software, automation tools, and security solutions that align with your specific needs and budget.

- Accounting Tech Tips Implementation Roadmap: We create customized implementation plans for these accounting tech tips based on your firm’s specific needs, budget, and timeline

- Seamless Cloud Migration and Management: Transitioning to cloud accounting requires careful planning and execution. GiaSpace provides end-to-end support for migrating your data and systems to secure cloud environments like Microsoft 365 and Azure, ensuring minimal disruption and maximum efficiency. We then offer ongoing managed cloud services to keep everything running smoothly.

- Robust Cybersecurity Implementation and Monitoring: Protecting your clients’ sensitive financial data is our top priority. We implement multi-layered cybersecurity solutions, including advanced threat detection, endpoint protection, multi-factor authentication, and employee security awareness training. Our 24/7 monitoring ensures your firm is protected against evolving cyber threats.

- Automation and Data Analytics Integration: We help you identify repetitive tasks ripe for automation and implement solutions that streamline bookkeeping, data entry, and reporting. Furthermore, we can assist in integrating data analytics and business intelligence tools to unlock deeper insights from your financial data.

- Secure Client Portal and Communication Solutions: We can help you select, implement, and optimize secure client portals and communication platforms that enhance collaboration, streamline document exchange, and elevate your client experience.

- Proactive IT Support and Management: Our managed IT services provide round-the-clock support, proactive monitoring, and rapid response times. This means your team can focus on their core accounting functions, knowing that any IT issues will be quickly resolved by our dedicated experts.

- Compliance Assistance: We stay updated on industry regulations and best practices, helping your firm implement IT solutions that support your compliance requirements and protect against legal liabilities.

Partner with GiaSpace to transform these accounting tech tips into measurable results. We’ve helped hundreds of accounting firms successfully implement these exact accounting tech tips, and we’re ready to create your customized roadmap. Don’t let these accounting tech tips remain theoretical—contact GiaSpace today to begin your technology transformation with expert guidance every step of the way.

Start with These Priority Accounting Tech Tips”

“Not sure where to begin? Our experience shows these accounting tech tips deliver the fastest ROI:

For Immediate Impact: Start with Accounting Tech Tip #3 (Cybersecurity). A single breach can devastate your practice, making this the most urgent of all accounting tech tips.

For Efficiency Gains: Implement Accounting Tech Tip #2 (Automation). Among productivity-focused accounting tech tips, automation delivers measurable time savings within weeks.

For Client Satisfaction: Deploy Accounting Tech Tip #5 (Client Portals). Of all client-facing accounting tech tips, secure portals generate the most positive feedback and retention impact.

GiaSpace can help you prioritize and execute these accounting tech tips in the optimal sequence for your specific situation.

Accounting Tech Tips: Frequently Asked Questions

What are the most important accounting tech tips for small firms?

The most critical accounting tech tips for small firms focus on cloud accounting software, automated bookkeeping, and robust cybersecurity. These accounting tech tips deliver immediate efficiency gains while protecting sensitive client data. Start with these foundational accounting tech tips before expanding to advanced analytics and AI solutions.

How much do these accounting tech tips cost to implement?

Implementation costs for these accounting tech tips vary by firm size and current infrastructure. Basic accounting tech tips like cloud migration and automation typically start at $500-2,000 monthly, while comprehensive accounting tech tips including advanced cybersecurity and AI tools may require $3,000-10,000+ monthly investments. However, these accounting tech tips typically deliver 3-5x ROI within the first year.

Which accounting tech tips should I prioritize first?

Prioritize accounting tech tips in this order: (1) Cybersecurity (protects your foundation), (2) Cloud migration (enables remote work), (3) Automation (frees up time), (4) Client portals (improves experience), (5) Data analytics (adds strategic value), (6) AI/ML (future-proofs operations). However, every firm’s priorities differ—GiaSpace can help sequence these accounting tech tips optimally for your situation.

Can accounting tech tips really improve client retention?

Absolutely. These accounting tech tips directly impact client satisfaction by providing faster response times, secure communication, real-time data access, and proactive advisory services. Firms implementing these accounting tech tips report 15-40% improvement in client retention and 20-60% increase in referrals within 12-18 months.

Do I need an IT partner to implement these accounting tech tips?

While some accounting tech tips can be self-implemented, most firms benefit from expert guidance. These accounting tech tips involve complex security configurations, data migrations, and integration challenges that specialized IT partners like GiaSpace handle more efficiently. Professional implementation of accounting tech tips reduces risk, accelerates deployment, and ensures optimal configuration.

Published: Jul 10, 2025

Need IT Support for Your Florida Business?

GiaSpace provides proactive managed IT services, cybersecurity, and local tech support across Florida — with teams in Gainesville, Fort Lauderdale, Jacksonville, and Ocala.

Managed IT Services FloridaCybersecurity Services FLGainesville IT ServicesFort Lauderdale IT Services